“Drill, baby, drill” ignited speculation on Big Oil’s upcoming performance during Trump’s recent inauguration, where he promised to lower energy prices by investing heavily in the oil industry. After the inauguration, Trump immediately declared a national energy emergency and cut down on Biden’s clean energy and vehicle policies.

On a logistic scale, the Trump administration will make it much easier for oil companies by increasing onshore oil production on federal lands, lifting Biden’s pause on liquified natural gas (LNG) exports, and increasing investments in Northern pipeline infrastructure. Especially concerning LNG exports, the Trump administration plans to take advantage of the 50% projected increase in global demand for LNGs. This spiking demand sparks from LNG’s potential to be more environmentally friendly than traditional fossil fuels, with countries like India showing the most significant interest in LNG exports.

Especially as the EV and clean energy industries are down after four years of the Biden administration supporting sustainability efforts, investors are beginning to bet big on prominent oil companies.

As of Wednesday, February 12, oil and gas companies British Petroleum (BP) and TotalEnergies SE (TTE) have experienced a 8.95% and 2.83% increase in share price performance since Trump’s inauguration, with other oil/energy stocks reflecting a similar trend. But will all these upward predictions for oil, gas, and pipeline businesses make them ‘drill, baby, drill’?

Despite investors' positive outlook, the petroleum growth ceiling depends on price and how willing big oil is to remain conservative with capital expenditures. Instead of frantically expanding drilling sites, the current industry prioritizes lower expenses with higher production rates. Of course, while Big Oil is thrilled that the Trump administration supports their initiatives, it merely simplifies the oil production process — which doesn’t necessarily incite petroleum companies to drill more. Not only are there still significant roadblocks in the production process that Trump’s executive orders can’t change (such as Federal eminent domain), but oil companies won’t invest any more in production unless they’re confident they’ll make money from the extra fuel churned out.

So, to encourage fossil fuel production for these companies and expand the drilling industry at the scale Trump wants, gas prices would have to rise significantly to counteract production expenses. As with any industry, a high price increase will expand production, while lower prices encourage companies to pull back. More expensive commodities discourage consumers, as we’ve seen with inflated prices.

Moreover, the industry must contend with global sanctions and lower oil prices, reducing the incentive to increase domestic production. Geopolitical tensions are significant when considering oil prices, which are currently variable to change as the Trump administration enacts tariffs against significant production and export destinations with negative attitudes towards clean energy (e.g., banning U.S. investments in Chinese energy firms).

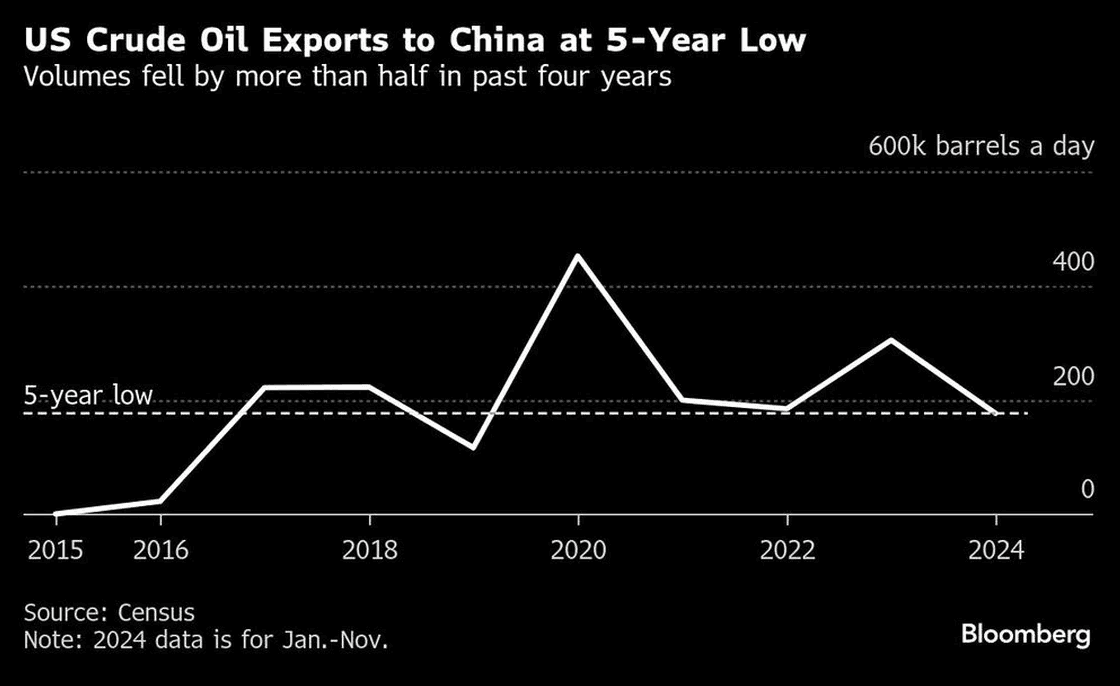

By late 2025, trade relations with major oil consumers such as China or India could lead to significant tanks or growth in oil prices. One major precursor to Chinese trade relations were 2018 tariffs that made many Chinese buyers reluctant to buy U.S. crude oil, which led to an $8 billion increase in the WTI-Brent discounts that year. Although a quarter of U.S. crude oil exports once went to China in late 2018, only 7% of that original amount now ends up in China, due to risk and implementation of tariffs. As shown in the figure below, the US is now witnessing the same decline in crude oil exports as China anticipated the return of Trump’s tariffs post-election day. While India is emerging as a potential trade partner for LNG (with a recent $10 billion contract signed between India and two LNG export terminals in Texas), it remains unclear whether United States will be able to rely on the projected growth for LNG exports in the coming years.

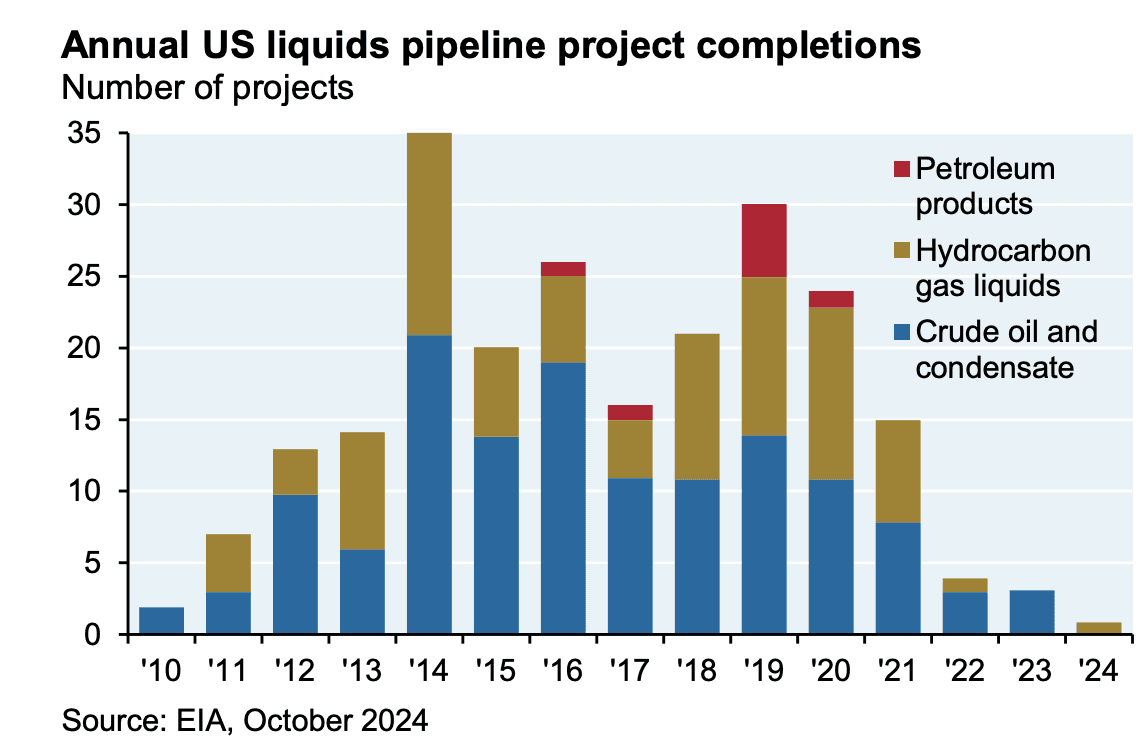

Another roadblock in the “lower oil prices, increased supply” plan is the challenges of expanding pipeline projects and increasing the capacity of an already booming crude oil industry. The Trump administration may remove challenges around obtaining permits, but it is an entirely different hurdle to create more drilling projects, without the government specifically setting aside domain legislation (or permission to drill on federal land). For the past few years, oil, gas, pipeline, and transmission projects have slowed to a halt (as shown in the figure below detailing pipeline project completions) — it would be a political miracle to restart projects at a grand scale. In other words, while crude oil exports have continued to match demand, companies aren’t willing to surpass already-high production costs by building more pipelines and drilling more wells. Therefore, oil exports are up, but production expansion is not. Finally, the United States has already been the leading crude oil exporter in the last five years, so increasing production to the scale Trump wants, demands a more saturated industry. Therefore, if Trump is trying to improve the oil industry supply, he’ll first have to confront the logistical challenges of pipeline projects and dedicate significant resources to revive pipeline project completions. Some of these logistical challenges are difficult to enact legislation against - such as land ownership disputes, federal permitting processes, and legal challenges from environmental/indigenous groups. In other words, we can expect that the ceiling has already been reached for how far the oil industry can grow.

Like many of the new administration’s policies, it’s difficult to determine whether Trump’s plan to invest in the oil industry will lower inflation rates and consumer prices. While the administration promises to develop the fossil fuel sector for our benefit, only the next few months will inform us whether Trump’s predictions ring true.

Trump’s first few weeks in office point towards positive growth for the oil industry. But, unless there is a significant incentive for these companies to expand production and LNG exports, investing in the fossil fuel industry now is risky, despite bullish outlooks. Trump may have eliminated the competition for clean energy with his recent policies. Still, unless he enacts legislation that removes all possible challenges to pipeline projects and provides incentives for oil companies to expand drilling projects, investors shouldn’t expect a considerable gain in the U.S. fossil fuel industry.